Stock Markets: Q3 Earnings Season Update

Uncertainties concerning the US and China trade negotiations remain an issue affecting business performance in the US. Out of this concern, the Fed cut interest rate in October 2019 by 0.25 percent. In terms of growth, the US GDP grew at a rate of 1.9 percent against a market expectation of 1.6 percent. The growth is a slight decline from 2.0 percent realized in Q2 of 2019. However, consumption by households grew to 2.9 percent while government spending increased by 2 percent.

The US economy performed better in Q3 compared to the rest of the world, as both the fixed income and equities earning were positive. Below are two highlights from the US third-quarter earnings results.

Stock Market Earnings Were Better Than Expected

Many analysts had expressed reservations regarding the third-quarter performance due to the current global economic slowdown and the China-US trade wars. The actual results from the Q3 period indicate that the markets have appreciated. An Increase in consumer spending resulted in a better than expected GDP for the third quarter

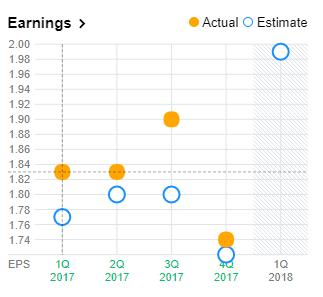

The S& P 500 is considered a good indicator of US stocks and business performance. To date, 91 percent of companies in the S&P 500 have reported their earnings. Seventy-three percent of these companies have reported better than expected per share. Historically, an average of 56 percent of companies usually achieves better than expected EPS. In terms of sales, 60 percent of the companies have reported figures above estimates, which is above the five-year average. The S&P 500 is on an uptrend throughout the third quarter. It gained 1.7 percent in that period. The index is now up by 20.9 percent in 2019; it’s the best-run since 1997.

Despite the positive earning, some analysts viewed the earning as a mixed bag. The aggregate net income for the companies that have reported so far is lower than in the net income of the same companies in previous periods. However, revenue growth is in a range previously achieved by this group of companies. For these companies, net income is down by 0.6 percent, while revenues are up by 4.9 percent.

US Economy Resilience to Tariffs and Wage Inflation

Trade wars between china and the US have seen the two countries impose steep tariffs upon each other. The depreciation of the Chinese Yuan countered a recent decision by the US to apply tariffs on more Chinese imports. The twists and turns that have characterized trade negotiations with China have not impacted the Q3 earnings significantly as initially feared. Although manufacturing dipped in Q3 2019, businesses still reported increased revenues.

For several months, the average hourly rate has been increasing steadily. While unemployment at its lowest level in decades, the wage rate is rising at a faster pace than inflation. For Q3, the annualized weekly wage rate rose to 3.3 percent. The rise was an improvement of a 2 percent increase in the second quarter. The increase in wages has not affected profits and earning to warrant a freeze on employment or layoffs.

Conclusion

In Q3, the earnings in the US appreciated. A Majority of companies forming the S&P 500 have reported a higher than expected EPS, better sales than the forecasts, or both. Businesses have proved resilience to rising wages, and the uncertainty brought about China and US trade wars.