Federal Reserve: Rising Risks for Recession in 2019?

In the last few months, the financial markets have experienced rising volatility. This activity has left many consumers on edge and wondering about the best ways to protect their assets. Recent commentaries from the Federal Reserve have also highlighted a growing possibility that the U.S. economy will experience recessionary conditions as early as next year.

Not surprisingly, this has already ignited speculation amongst some analysts that the current environment could be causing another financial collapse similar to what was seen during the 2008 financial crisis.

Of course, much of this speculation is still premature as growth numbers throughout the U.S. remain robust and consumer spending levels are firmly above those which characterized the periods following the credit crunch a decade ago. But there are still factors which households and individual consumers should consider when making plans for investment or spending money as part of a daily routine.

Effects of Interest Rates and Rising Consumer Costs

In all of the chatter (which has drawn similarities between the financial environment of 2008 and the financial environment of 2018), many people have neglected the ways higher interest rates could impact economic growth —at both the micro and macro levels.

But this might turn out to the most critical factor which has changed the market this year. The prospect of higher interest rates can have a major impact on the economics of the stock market and this type of activity has already cost investors a great deal of money with respect to this year’s investment returns.

Additionally, higher interest rates can make large purchases more expensive for households. For example, mortgage lending rates have risen to their highest levels in years and similar trends can be seen in the costs associated with the ability to buy a new automobile.

For those that are able to buy a home or a car outright, these types of scenarios have limited impact on spending practices. But the majority of households and consumers do not fall into this category and this means that an environment of rising interest rates will have a very real impact on the financial health of most people.

U.S. Economics: Focusing on What Matters

For all of these reasons, it is important for us to focus on what matters and it is never a good idea to dismiss the underlying trends which are being developed by the Federal Reserve. These are concepts which might seem to be abstract and esoteric. But this could not be further from the truth, as steadily rising interest rates have a very real impact on the ways we structure our long-term purchases.

Since the continued prospects of higher interest rates make large purchases more expensive, it might make sense to complete some of these purchases before the rate cycle reaches its maximum peak. So, for example, if a family is considering putting off the purchase of a new home until next year, it might actually make more sense to speed-up the timeline and consider alternative options sooner.

Stock Markets: Long Term Economic Trends

In the long run, these types of decision planning practices can have a substantial impact on the monthly payment and total costs which are required of us. Most financial decisions which are made quickly and impatiently tend to cost more over the long-term, and when we make too many of these decisions it is all too common to see the final outcome rest in bankruptcy.

This is why macroeconomic changes matter and the daily fluctuations in the financial news headlines usually do not matter (at least, not as much). With this in mind, consumers can probably look past the speculation that a financial collapse is around the corner. But this does not imply the economy “without risk” is an accurate depiction of the current landscape.

Financial Planning: Choosing Between Stocks or Bonds for Your Retirement Account

“Behold the turtle. He makes progress only when he sticks his neck out.” — James Bryant Conant

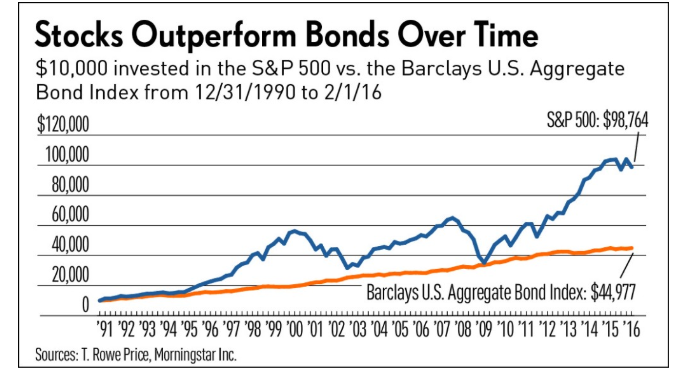

If you are planning for retirement, you have probably felt the pressures involved when looking at all of the different places to park your money. The financial landscape can be a complicated place, and the task of choosing between asset classes can seem daunting during the early stages of the process. Two of the most popular asset classes are stocks and bonds, and many newer investors often wonder which is best for a long-term retirement portfolio.

In any retirement portfolio, investors must understand the concept of market risk as it relates to their positions. This essentially refers to the possibility of losses relative to the potential for reward (gains) in the investment. These factors work hand-in-hand, but a seasoned financial advisor can help understand the nuances which are present when planning for retirement. We sat down with Adam Anderson, CEO of MRA Capital Partners to identify new strategies to turn the odds into our favor on the path toward building wealth. Below, we can find some tips we uncovered along the way.

Measuring Potential Returns

As a general rule, greater potential for gain tends to be associated with larger levels of risk. These factors can be understood when comparing the historical returns generated by investments in both stocks and bonds. When a retirement portfolio is designed by an industry expert and assets are properly allocated, risk is generally a short-term phenomenon. The potential for returns differs when we are comparing the advantages of stocks and bonds, and the appropriate selections for your retirement portfolio will depend heavily on your individual goals and needs.

Over the last century, U.S. Treasury Bills have acted as a proxy for money market accounts (generating yields of roughly 3.7% annually). Longer-term government bonds returns about 5.7% over the same period. Put in simple terms, if you invested $1 in long-term bonds in 1926 your investment would be worth about $100 in 2008. Stock investments, on the other hand, would have produced very different results (generating annual returns of 9.6% during these same periods). In this case, a $1 investment in large-cap stocks in 1926 would be worth about $2,000 just prior to the financial turmoil of 2008.

In the chart above, we can see the more recent trends in stock markets as they relate to the bond markets. Interestingly, there are some cases where the traditional correlations to not match the current tendencies. These asset classes have had periods characterized by similar returns (both small and large). This is precisely why retirement investors will consult an experienced financial advisor, so that it is easier to spot the differences in any given market climate.

“As a CFP and Financial Planner, I’ve practiced the principles of asset allocation and diversification through both bull and bear market cycles as well as expansion, contraction, and recessionary economic climates. Diversification between asset classes is paramount to a successful investment strategy,” Mr. Anderson explained.

“At the most broad level, the mix between stocks and bonds is most commonly debated especially among retail investors and their advisors. In my opinion, the most heavily overlooked asset class for individual investors are alternatives. Alternatives can be commodities, futures, real estate, private equity, art and other non stock or bond investments. Alternatives should make up between 10%-20% of a well diversified portfolio for the average investor but is much higher for some institutional investors, endowments, pensions and high net worth individuals. While I don’t personally endorse this, some even choose to invest only in non market based alternatives ignoring stocks and bonds completely,” Mr. Anderson explained.

“The benefit to alternatives is that when managed correctly, they should be non-correlated to stocks or bonds. Private equity and Real Estate tend to do a very good job at this. The challenge is finding the right managers and strategies that fit the investors goals and comfort level. Another challenge is investment minimums are generally very high and transparency is generally low when investing directly in real estate for example,” Mr. Anderson explained.

MRA Capital Partners seeks to remove these barriers by offering limited partnership interests in a variety of single asset real estate investments as well as its Lighthouse Fund which is a diversified pool of high yield asset backed loans. The individual accredited investor can access these private non-correlated investments for as little as $50,000 and has full transparency via our secure investor portal at www.mracapitalpartners.com.

Limiting Risk in Retirement Portfolios

More broadly, stock markets have generated much higher average returns, and this is why retirement portfolios tend to be more heavily-centered in these areas. Of course, this added potential for return comes with added risk for the investment. But since the stock market tends to post positive results during the vast majority of market scenarios, any losses tend to be removed over time.

These are all risks which must be understood but when we have a well-constructed investment portfolio it becomes possible to turn the odds in our favor. Markets will always experience -boom-and-bust type periods in the broader economic cycle. But when a retirement portfolio is well-constructed and diversified, these risks can be mitigated and substantially reduced. Stock markets move higher during the vast majority of the time, and this is why buy-and-hold strategies tend to work best in generating returns and investment income.

“Heading into 2019, it’s no secret we are in the later stages of the current economic expansion and the federal reserve has made it very clear they plan to continue on their current path of raising rates. This along with the uncertainty surrounding the current political and trade headline risk is likely to continue to cause volatility in the stock and bond markets,” Mr. Anderson explained.

“If rates rise more rapidly than anticipated, bonds may prove to be less of a safe haven or diversifier than investors expected. Additionally, as the world economy continues to become more integrated, many of the more liquid asset classes like stocks, bonds, REITS, and even liquid alternatives like those access via ETFS or Mutual Fund may prove to be more correlated to each other then they have been in the past. In my opinion, carefully selected privately held investments are the best way to gain non-correlated exposure,” Mr. Anderson explained.

Understanding Time Horizons

Time is another important factor in any investment. Will you be retiring 10 years from now? Twenty years? Maybe much sooner? It is never too late to start planning your retirement portfolio. But the time you have until you stop working your regular job can be an important factor in determining which types of assets to include in your investment portfolio. If you have an extend time period before your retirement, there is often better opportunity for capital growth through stock investments. Conversely, if you are looking for short-term stability and income, bonds may offer advantages given your individual needs.

“There are risks associated with all investments. At MRA Capital Partners, we focus on privately held investments back by the hard asset of real estate. While these types of private equity and debt investments are not immune recessions, rising rates and other market forces, they very rarely behave like traditional stocks or bonds which may be a great complement to a balanced portfolio. Additionally, investments offered by MRA Capital Partners have a strong income component, many distributing 10% or more annually which make them a great complement or even alternative to bonds,” Mr. Anderson explained.

Of course, these are all factors which should be discussed with your investment advisor, and the answers will differ depending on your individual needs and goals. There is no substitute for individual attention and it must always be understood that “patience pays” in any financial markets investment. As the sage wisdom of James Bryant Conant tells us “Behold the turtle. He makes progress only when he sticks his neck out.” This suggests a certain level of risk can be taken, as long as those risks are measured and characterized by patience that is well-researched in the current market environment.

For this article, we interviewed Adam Anderson, CFP®, CRPC® CEO – Managing Partner of MRA Capital Partners.

Closed-end Funds: Global Exposure In The Asia Pacific Fund

The Asia Pacific Fund, Inc (NYSE: APB) is registered as a closed-end management investment company, with an objective to achieve long-term capital appreciation through investment in Asia Pacific Countries (excluding Japan). This creates the opportunity for investors to gain access to emerging markets throughout the region while still maintaining broad regional diversification.

Source: CEF Connect

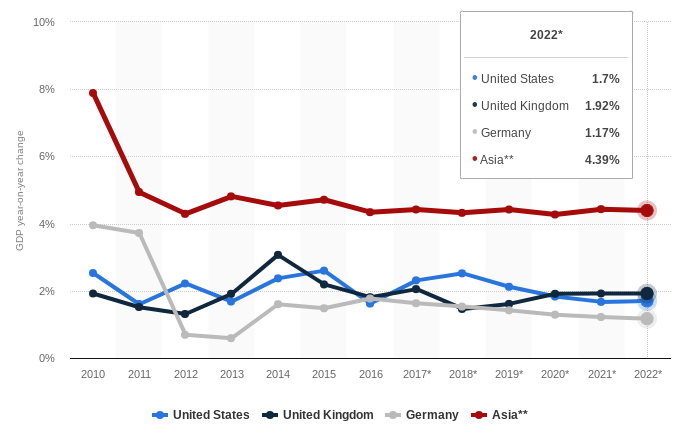

Most analysts agree that a significant portion of global growth will be present in emerging Asia over the next decade. These assets can be accessed at cheaper levels given the Asia Pacific Fund’s attractive discount to net asset value (NAV). The fund has rallied strongly since February 2016, and investments here come with an attractive dividend yield of 2.14%.

Economic Trends in Asia

The year 2017 was positive for Asian markets. Stocks throughout the region recovered against the backdrop of upward revisions in earnings and stabilizing political factors externally. The MSCI Asia All-Country Index (which excludes Japan) closed with a 42.1% gain for the year, and its dividend yield index rose by 29.8%. The rising tide lifted many regional funds, and this positivity in global markets helped the Asia-Pacific Fund gain approximately 50% in 2017.

The MSCI Asia All-Country Index (which excludes Japan) closed with a 42.1% gain for the year, and its dividend yield index rose by 29.8%. The rising tide lifted many regional funds, and this positivity in global markets helped the Asia-Pacific Fund gain approximately 50% in 2017. These are strong gains which are more closely in line with the longer-term expectations for Asia (relative to Western economies) through the year 2022.

Source: IMF

However, shorter-term volatility has remained in place, and the first quarter of 2018 was not as expected. In the wake of faster-then-expected interest rate hikes by the US Fed Reserve, investors enacted strategies tied to risk aversion.

The world also saw itself on a brink of a trade war between the U.S. and China, which hastened with widespread tariff implementations. The Asia-Pacific Fund fell 0.9% during the period extending from January 2 to April 2, 2018. The greatest drop in the share prices was between January 31 and February 12, wherein the stocks plunged by 10% before entering correction territory in the next few days.

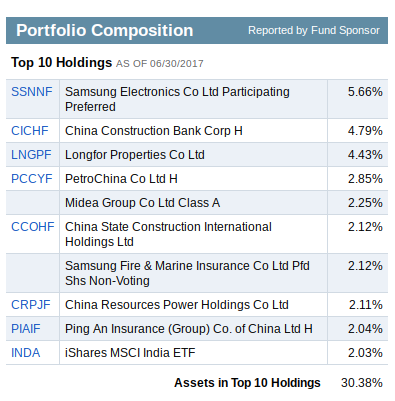

Fund Holdings

The reality is that as interest rates have increased in Asia, liquidity has tightened. Even though the NAV and the market price of the Asia-Pacific Fund both increased by more than 20%, the year its share of challenges.

Problematic sectors were seen in the internet and software industry. To mitigate the negative influence of global trends, the Asia-Pacific Fund has balanced its portfolio to increase exposure to top performing sectors (like industrials, information technology hardware, and real estate).

Source: Fidelity

The major sector concentrations of the fund are devoted to Real Estate (17.7%), Industrials (16.2%) and Consumer Discretionary assets (15.9%), with 5% given to holdings in both Longfor Properties Company and China Construction Bank (Class “H” Shares).

Financial Performance

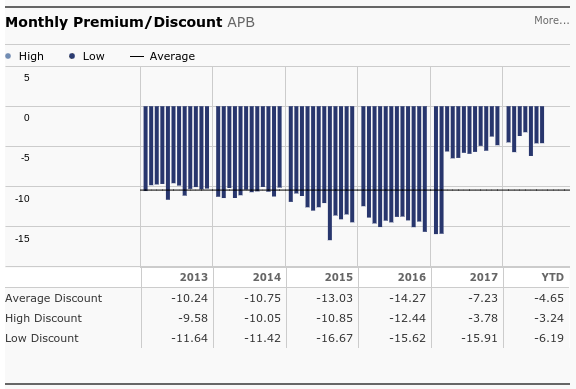

The overall performance of the fund was positive during its annual period ending on March 31, 2018. The Asia-Pacific Fund shows that price-to-book multiples, price-to-earnings multiples and its yield remain favorable when compared to the benchmark MSCI AC Asia Index (ex-Japan). Positive developments in this regard prompted the Board to advise shareholders to vote against the proposed liquidation of the fund.

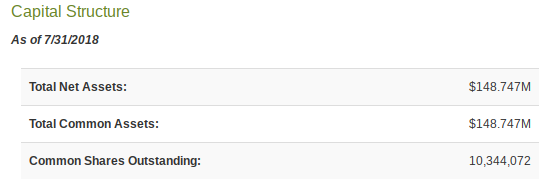

This looks to have been a wise choice given the subsequent performance seen in share prices. Currently, the Asia-Pacific Fund has total net assets of $148.8 million and has 10.3 million outstanding shares as of July 31, 2018. The net asset value stands at $14.38 and a commitment to its Dividend Reinvestment Program is what makes APB a favorable option for prudent investors.

Source: Morningstar

The fund’s NAV per share has increased from $12.96 on March 31, 2017, which means we have seen gains of nearly 11%. On December 21, 2017, the fund paid out a dividend of $0.61 per share (with a yield of 2.11%). The PE Ratio stands at 4.53 and the EPS is $3.2. For the Asia-Pacific Fund, the momentum in earnings revisions has acted as a key driver of growth.Investors can look forward to a potential growth in the stock prices as the fund has posted a consistent performance over the past two years.

After facing a drop in February 2016, the stock raised back by 75% in the period ending November 2017. The increase in the stock was due primarily to the positive performances seen in the real estate and hardware sectors. This suggests that markets are well-prepared to buy the stock when it is trading at a significant discount. The positive performance and economic growth of the Asia Pacific region continues to have a positive impact on share prices – and this looks set to continue in the quarters ahead.

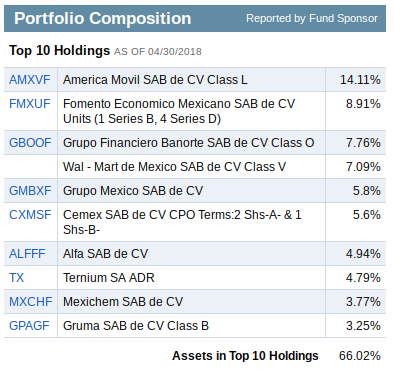

Mexico Fund: Stable Exposure To LATAM Emerging Markets

The Mexico Fund (NYSE:MXF) is a closed-end fund designed with the investment objective of providing long-term capital appreciation through strategic portfolio allocations in the markets. Incorporated in June 1981, and domiciled in the U.S., has always been managed by Impulsora del Fondo Mexico S.C. The fund offers well-positioned access to Mexico’s economy through a broad range of public listed companies.

Economic Trends in Mexico

Since MXF mainly offers exposure to equities securities listed on the Mexican Stock Exchange, the economy of Mexico has a substantial impact on the fund. However, several of these companies now earn a significant portion of its income and profits abroad, through exports and subsidiaries in other countries or regions. Broadly speaking, the macro trends look highly encouraging.

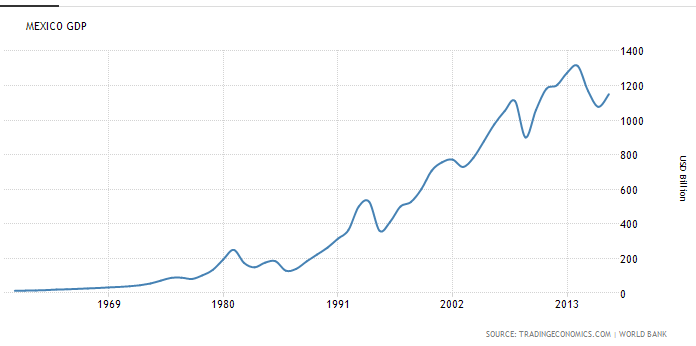

Economic: Mexico GDP

Source: World Bank / Trading Economics

In 2017, the economy of Mexico grew at a rate of 2%, while in the first half of 2018 the pace maintain the 2% rate. Analyst surveys at the Mexican Central Bank predict sustained full-year expansion of 2.3% and 2.2% for 2018 and 2019, respectively.

Political uncertainty due to Presidential elections held on July 1st 2018, and the significant volatility seen in the global stock exchanges earlier this year had a visible impact on the share prices of MXF. Share prices reached its yearly low on June, however, the stock has posted a sharp bullish reversal, and this suggests that a long-term bottom is likely in place for the stock.

The prior negative trends in the stock price can be attributed to strong movements in the global environment. Some of the major events that have impacting the MXF fund during this period:

Sharp decrease in oil and other commodity prices staring on 2014.

Political environment in the U.S.

Pending resolution of NAFTA renegotiations.

Political uncertainty in Mexico due to Presidential elections.

Finding Opportunities At Lower Valuations

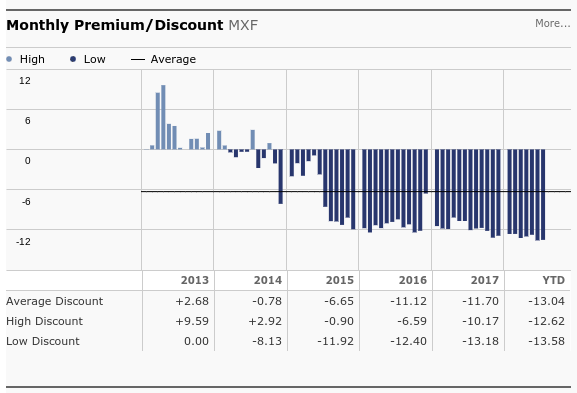

Macro trends over the last few years have not been favorable for regional assets. But these declines have created significant opportunities for investors. When viewing the closed-end fund through the lens of its discount to net asset value (NAV), we can see that the Mexico Fund is now trading at some of the deepest discounts in its recent history.

Source: Morningstar

On June 12, 2018, the Board announced a dividend of $0.15 per share to its investors. This represents an annualized dividend of $0.60 per share, and an accompanying dividend yield of 3.63%. The quarterly dividend was increased from $0.13 per share to $0.15 per share in April 2018, representing an increase of 15.38%.

Source: Fidelity

During the first seven months of 2018, the Mexico Fund has had a productive year, with a positive NAV total return of 8.78%, while outperformed its benchmark (the MSCI Mexico Index) by 250 basis points. As of July 31, 2018, the fund’s market price was $16.63 and its NAV per share was $19.23. The Fund has outperformed its benchmark during the last one, three, five and ten year periods ended on July 31, 2018.

Positive Improvements in Share Prices

During the May-June period this year, the broader market experienced the broader ramifications of the ongoing trade-war tussle between the U.S. and China. The Mexico Fund saw a nice rebound following this period, however, and the stock correction generated gains of 13% through mid-July. This creates a more positive outlook for the remainder of 2018, as trade war fears have subsided, global trade exchanges have resumed their previous rallies and an improved political environment.

Fund Exposure

Changes in fund holdings in the first half of 2018 have created additional positives, as exposure in the domestic consumption sector was reduced in favor of increases in exposure to the financial services sector. Widespread gains have been seen in financial stocks over the last year, and this puts the Mexico Fund in a much better to capitalize on those trends going forward.

The rising cost of raw materials and high relative valuations have impacted the profitability of companies in the domestic consumption sector, while the financial services sector is still showing higher projected margins. All together, this bodes well for the outlook and sets the Mexico Fund on a course to close its NAV discount heading into next year.

Brookfield Real Assets Income Fund Set to Move Higher

In December 2016, Brookfield Asset Management merged three of its funds (HHY, HTR and BOI) to form the combined Brookfield Real Assets Income Fund (NYSE:RA). Since then, RA has helped raise Brookfield’s profile in the asset management sector and infused flexibility into the fund’s asset allocation. RA is also showing signs that a bullish reversal has been in place since the middle of March.

Stock Chart

The three original funds had a focus largely on debt. But these more recent moves have allowed Brookfield to pursue a more dynamic approach, allowing investment decisions to be dictated more closely by the changing needs of the market.

Stock Chart

The fund’s elder sibling is the Brookfield Global Listed Infrastructure Income Fund (NYSE:INF), which was formed way back in August 2011. When looking more deeply into the fund, we can see that 80% of its managed assets are in publicly-traded securities tied to companies in the infrastructure sector. INF has $196.46 million worth of assets under management, and the stock has moved steadily higher since the beginning of 2016.

Impact of Political Upheavals and Monetary Policy

As is the case with most of the market, the impact of political upheavals on these stocks should not be ignored. We are still seeing escalating trade tensions between US, China, and the Eurozone – and this is having a rippling effect throughout stock exchanges across the globe. This generated many of the declines experienced in stocks such as RA and INF during the month of March 2018.

Ultimately, those declines can be viewed as new buying opportunities for the stock. In March, RA saw a steep drop in share prices, falling by 9.9% from its earlier highs of $23.93 in January. To a large extent, these bearish moves can be attributed to the panic felt by investors which relates to potential interest rate increases at the Federal Reserve. This was especially true after the release of January’s nonfarm payrolls report.

Deeper NAV Discounts and Higher Returns

On a YTD basis, RA is trading lower by -2.14% and INF has shown losses of -4.8% over the same period. This creates added discounts for investors relative to net asset values.With $888.3 million in net assets, RA has consistently generated higher returns through current income values and capital growth. RA’s most recent monthly distribution was $0.1990 per share and its NAV discount currently stands at 5.29%.

Stock Chart

RA’s weighted average duration of 1.4 years is another positive sign for the prudent investors. When considering the rate of inflation and the consistently upward path of interest rates, it is important to understand that there will be repricing effects in most of the fund’s assets. As rates go up, RA stands to gain (due to its weighted average period).

On the negative side, the Undistributed Net Investment Income (UNII) for the stock should be noted. Since UNII is a direct indicator of dividend payment availability, investors focused on income might highlight the possibility that Brookfield will have distribution difficulties. However, when looking at the larger picture, we must understand that roughly 41% of all closed-end funds have a negative UNII. In the case of RA, this risk is partially mitigated as a portion of its current portfolio is devoted to infrastructure companies that pay their distributions as return-on-capital.

Elevated Dividend Yields

In all likelihood, the fund could continue to attract income investors because of its elevated payouts. RA offers broad exposure to U.S. and International securities with investments in high-yield and floating-rate debt assets. The stock yields 10.43% at current price levels ($2.39 per share). This creates some interesting opportunities for value investors given the recent declines in share prices. The promise of elevated income and a diversification into real assets helps RA stand out in the current market environment.

Similar characterizations can be made in relation to INF, which most recently paid a monthly distribution of $0.817. On an annualized basis, this represents a dividend payout of $0.98 per share, and a percentage yield of 7.94%. As the stock continues on its positive trend, broader sentiment seems to be falling in line with expectations. Accern Sentiment Analysis is now seen giving the stock a positive score of 0.15 on the Accern scale.

All together, the outlook looks stable and investors should consider RA as a steady option in closed-end funds that is prepared to capitalize on its four core advantages: portfolio diversification, a closing discount to NAV, strong probabilities for capital appreciation, and its elevated dividend yields for income investors.

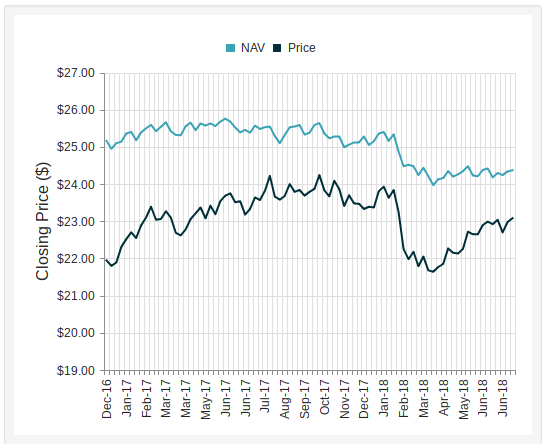

Equus Total Return Offers Opportunities in Small-Cap Stocks

Stock markets continue to push higher after the volatile and problematic trading activity earlier this year. The S&P 500 is breaking to new highs above 2800 and investors looking for value have found it increasingly difficult to locate stable stock opportunities that are still trading at favorable valuations. But one area that should continue to be on the radar for investors is the small-cap space, as there are many excellent pockets which be found in key industry sectors.

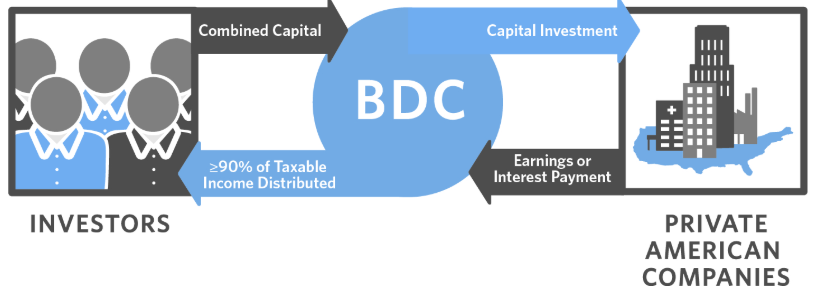

One key stock selection is Equus Total Return, Inc. (NYSE: EQS), a business development company (BDC) which was formed with the aim of generating superior overall returns through current income and capital appreciation investment strategies. This objective is accomplished by investing in equity and debt securities in companies with a total enterprise value of between $5 million and $75 million. As a BDC, Equus is required to invest 70% of its assets in private and small public U.S. companies.

In addition, Equus qualifies as a Regulated Investment Company (RIC) under the Internal Revenue Code and does not pay corporate income taxes, so the combination of these factors brings stability and cost-value for sustainable growth positioning in the market.

Assessing the Market Outlook

In March 2018, the U.S. Federal Reserve raised its benchmark interest rate (by 0.25%, to a target range of 1.5% to 1.75%). This decision was accompanied by an announcement of at least two more planned rate hikes before the end of the year. This shift in monetary policy has prompted the Equus board to review its investment strategies and seek opportunities for liquidity in certain aspects of its portfolio as a means of enhancing shareholder value.

Undeniably, global economic events have had an impact on Equus shares and on the stock market as a whole. The 2015-16 equities sell-off, promulgated by Greece’s default on its debt securities, the collapse of oil prices, and an overall downturn in the broader economy, led to rising volatility on Wall Street. But when we view the broader trend activity in the stock, we can see that Equus held up surprisingly well under the circumstances.

As this occurred, the price of Equus shares declined by roughly 30% (from its high of $2.45 in January 2014 to $1.50 in March 2016). The stock then rose by 90% in May 2018 before giving back some of those gains again in June of the same year. This latest round of macro volatility was brought about by the ongoing trade war discussions between the U.S., China, and the Eurozone.

Equus: Assessing the Financial Metrics

When assessing the financial metrics, several key positives can be seen. Revenues for 2017 came in at $3.7 million, which was a gain of more than 400% on an annualized basis. These achievements were due, in large part, to the strong performance of its portfolio company MVC Capital. Operating cash flows stood at $10.0 million, and those performances may have been even more impressive if the planned merger with U.S. Gas & Electric had reached completion.

Looking ahead, these positives are flashing potential ‘buy’ signals for investors based on the growing likelihood the Equus stock will see a narrowing in its discount to its net asset value (NAV). With its current share price of $2.28, the stock’s P/E ratio has fallen more in line with the averages seen for the financial services sector (now at 19.70).

Equus Portfolio Positioning

Looking at specific portfolio positioning, the fair value of its holdings in Equus Energy have increased from $6.3 million to $8.0 million, due to the positive developments in economic conditions that impacted mineral rights owned by the company. With ownership of about 144 producing and non-producing oil wells, Equus Energy has a strong outlook for further development.

During 2017, the fair value of Equus’ share interest in PalletOne increased from $16.2 million to $16.7 million, due to overall improvements in the wood products and packaging industry, as well as the specific financial performance of PalletOne during the year. PalletOne is the largest wooden pallet manufacturer in the U.S. EQS holds an 18.7% equity share in this key industry asset.

Lastly, the fair value of Equus’ share interest in MVC Capital increased from $4.0 million to $5.2 million. The trading price of MVC’s common stock rose from $8.58 per share in 2016, to $10.56 per share in 2017. MVC also paid Equus a dividend of 27,600 shares during this period. This increase in the MVC share price and dividend payouts helped improve the relative position of Equus’ portfolio holdings – and this helps brighten the outlook for investors.

Bouncing Back from Merger Obstacles

The Equus trading price suffered a hit after the merger agreement with U.S. Gas & Electric was terminated in May 2017. The merger was designed as a stepping stone in its reorganization plans, but the initial declines quickly corrected it in the days that followed. A termination fee of $2.5 million received by Equus has positively impacted the company’s available cash balance, and any resulting declines in stock prices are now being viewed as new buying opportunities.

Overall, it is clear investor sentiment has turned positive for Equus. Elevated valuations in the S&P 500 suggest that investors should be looking to small-caps (and at closed-end funds, in particular) when seeking value in this context. The stock’s attractive NAV discount and solid positioning within the industry suggest we will probably see further gains in share prices. For patient investors, Equus has shown the ability to streamline its portfolio exposure in ways that are expected to benefit shareholders in the quarters ahead.

Stock Markets: Global Trade Summit Could Change Investor Sentiment

The first half of 2018 has proved to be an average year for DIA index compared to the first half of 2017. DIA is down by 2.16% (YTD), while in 2017 it was up by 7% during the same period. It has a dividend yield of 1.86% and an annualized payout of $4.52. The annualized growth in the last three years was 9.6% with a growth of 7% in 2017.

AUSTRALIAN ASX 200

The current half of 2018 has seen its own mix of political and economic upheavals thus bringing in serious volatility in all the exchanges around the world. The events that caused headwinds were the historic meeting between President Donald Trump and President Kim Jong Un of North Korea and, the G-7 Summit.

Macro factors continue to dominate the investment news headlines, and this is unlikely to change any time soon (as long as the trade war discussions are widely covered in the financial media).

How is global trade affecting performance in 2018?

The graph of DIA has been showing substantial ups and downs in the first half of 2018 due to the impending fears of a trade war and the federal interest rate hike.

In mid-June, the stock tumbled down 1% on the wake of President Trump’s threat of imposing tariffs on $200 billion worth of Chinese products. The major stocks to be hit were Boeing (BA) and Caterpillar (CAT) which dropped by 4% each. Goldman Sachs (GS) was up by 0.9%, 3M (MMM) was up by 0.6% and Home Depot, Inc (HD) was down by 0.3%.

Dow Jones Industrial Average

The DIA index fell down from its 50-day moving average. Compared with S&P 500, DIA has been seeing a downtrend mirroring the performance of Dow Industrials. It is a signal that DIA would thus be weaker than SPY and S&P 500. The tariffs would come in force on July 6; however, its impact on the broader exchange market is yet to be seen. In the meantime, the trade war continues between US, China, and the Eurozone markets.

Trends in stock market ETFs

DIA, like other ETF’s, showed a positive growth in June 2018 due to the recently released job data and falling unemployment rates. The greatest shock to the Dow Jones Industrials was the removal of General Electric, the longs standing and continuous member since 1907.

In the DIA, Boeing had a weight of 10% in the index, while General Electric was 0.35%. Wallgreens Boots Alliance Inc (WBA) entered as the replacement stock on June 26. The removal of GE will have a big impact on thousands of investors who have holdings in the Dow Jones.

All in all, the stock market is now in precarious territory and investors in assets like the SPDR Dow Jones Industrial Average ETF will need to remain nimble (and attentive to economic data) in the weeks and months ahead.

Australian equities markets

After facing considerable plunges during February and March 2018, the shares of S&P/ASX 200 showed substantial volatility during the first six months of 2018 after settling down with a YTD growth of 2.2%. The Index had shown a steady growth of 7% in October 2017 ($6,029) against the backdrop of the positivity brought by the announcement of the US tax cuts. This growth remained steady till February 2, 2018 ($6,121), when the S&P/ASX 200 fell down 4.7% in the next two days.

The Index plunged by 5% or 300 points during the period from February 2 ($6,121) – February 12 ($5,820). The stocks fell due to nasty selling by the investors due to the fear of an increase in the interest rates followed by the testimony from new Fed Chief Jerome Powell.

February 5 was the worst day for the index since June 2017 as prices fell 95 points or 1.6%. This was primarily due to the release of the US jobs data. The wage data led to panic among investors that interest rate hike was likely too. This uncertainty coupled with the inflation fears started the market rout on Wall Street which then affected other exchanges across the globe. The Australian dollar too touched an all-time two-month low.

Banking stocks

The stocks, however, rebounded back in the coming weeks by 4% after National Bank of Australia (ASX: NAB) posted an increase of 3% in the first quarter profits. Following NAB was AMP Limited which posted an increase of 24% in its revenue, while Mirvac Group and AGL Energy both posting an increase of 8% and 7% in its half-year revenue.

In March 2018, the ASX 200 dropped another 5% (February 27 – March 29) due to the US-China trade war. This heavily impacted the Wall Street and spiraled across Asia leading to a fall in the ASX 200 and All Ordinaries, with Banks and the Miners taking the biggest hit in this debacle. However, the market gained momentum in April helped by the rising commodity prices and positive growth in the Energy (+10.7%) and Materials (+7.4%) sector.

From its all-time 2018 low of $5,751 on April 3, it shot up to $6,225 on June 22, an increase of 8.35%. This was particularly due to key global events like the meeting of the President of the US and North Korea and the updates on the jobs growth in Australia and China. June 15 was termed as the best day in the ASX, as All Ordinaries saw a growth of 1.2%, while ASX 200 grew by 1.3%.

Citigroup: Stock Undeterred by a Hefty Tax Charge of $22 Billion

As a global banking leader for more than 20 years, Citigroup, Inc. (NYSE: C) posted a net income (on an operating basis) of $15.8bn in 2017 with an EPS of $1.28, 12% higher from 2016. This was the first time since the financial crisis of 2008 where earnings are more than their expectations.

The stock rallied to an all-time 10 year high of $80 on January 26, 2018. Total revenues in 2017 were up by 2%. Citi took a one time charge of $22bn (including $3bn in the repatriation of foreign funds) due to the Republican tax reform policy.

Citi stock is a favorite for shareholders and prospective investors as it has a steady EPS growth and is the cheapest of all banking stocks in the market. It is by far the largest of the top 10 banks in terms of EPS growth and P/E (according to Bloomberg Consensus). In terms of valuation, its stock is trading at a 22% discount and has a growing yield in its Corporate and Treasury bonds.

Source: Google Finance

With a good performance in 2017, it is now noticeable that Citi has come out the volatile period of revenue growth. Even after getting hit by a $22bn tax charge, Citigroup stock rose by 1%, as it delivered good performance excluding the charge. The new tax rate will give a boost to its profits.

Along with this, Citigroup CEO has reiterated on its promise of returning at least $60bn to investors in the next few years through buyback and dividends.

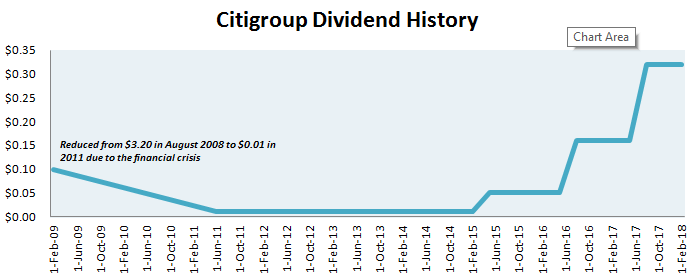

Citigroup Dividends: An Interesting Tale

Citigroup Dividend History

On January 18, 2018, Citigroup doubled its dividend of $0.16 to $0.32 after receiving Fed approval for its $15.6bn share buyback program. This is the largest ever share repurchase announced by Citi since its 2005 buyback of $15bn. In June 2016, Citigroup had boosted its dividends to $0.16 from $0.05 – a total three-fold rise.

Prior to the financial depression in 2008-09, Citigroup was known for paying high dividends to the tune of $5.4 per share. During the crisis, it slashed its dividend down to $0.1 in February 2009 and did not pay any till June 2011. Post this, it kept its payout at a minuscule $0.01 till 2015 when it finally raised it to $0.05. Its current dividend yield is 1.88% and shareholders can expect an upward momentum in his regard.

Where Does Citi Stand with other Top Banks?

Source: NASDAQ

Comparing Citigroup with Bank of America, both have performed well in terms of their stock rise in 2017. Citigroup has increased 15% while Bank of America has grown by 26%. Citi’s forward earnings multiple is less than 10 while BAC is at 11%. Both banks provide a decent dividend yield of more than 1.5%, with Citi’s slightly higher at 1.87%. This makes Citigroup a better buy.

The impending trade war due to Trump’s policy also had an impact on Citigroup shares due to its geographic exposures (it has banking licenses in more than 100 countries). Hence, its stock growth was down last year compared to JPMorgan Chase (NYSE: JPM) and Bank of America (NYSE: BAC).

General Mills (GIS)beat earnings and revenue estimates with adjusted quarterly profits of 79 cents per share (78 cents expected). Stock prices fell sharply, however, as General Mills lowered its adjusted earnings growth forecast (to a range of 0% to 1%). The company’s previous forecasts called for much higher gains (within a range of 3% to 4%). Increased cost pressures were cited by the company as the cause for decline, and this is a bit ironic (or problematic) given the fact that prices could rise further as a result of heightened trade tariff talks.

Fundamentally, this puts the company at risk – and those risks look to be making themselves apparent on the technical charts.

Entertainment Stocks: Disney Will Buy Marvel Comics for $4 Billion

Stock market activity continues to be sluggish in most sectors but we are now starting to see more activity in the consumer entertainment sector. This month, we learned that Walt Disney Co. (NYSE:DIS) will buy Marvel Comics for $4 billion in a move to diversify its content base. The company hopes to expand its outreach in age demographics in order to shield against potential declines in other areas of its businesses.

More recent news of sexual misconduct from one of Marvel’s founding members, Stan Lee, could impact the timing of the deal, according to analysts. Disney has had a much-storied run over the last year, and the injection of negative media headlines could prove to be ill-timed as far as the investor outlook is concerned.

Source: CEF Connect

Source: CEF Connect

Source: Fidelity

Source: Fidelity

Source: Fidelity

Source: Fidelity