Procter & Gamble (NYSE: PG) stock had slid 9.92% in February 2018 after its Q2 2018 earnings release on January 23, 2018. A tantalizing problem for this Household and Consumer products giant was its performance in terms of market share. For blades and razors, the share was down to 65% from 70% in 2014 while grooming products dropped by 0.7%.

As revealed in its 2017 fiscal year-end results, the overall market share was declining across each of its core product categories. With regards the competitive edge, P&G is not immune to the intense headwinds in the market which has brought stagnancy to its top line growth in the recent years. Its market share was also impacted due to the niche operators in the household sector. However, the situation is now improving as can be seen from its 2% rise in organic sales.

The Q2 2018 results beat Wall Street estimates as it posted revenue of $17.40bn against the expected $17.39bn and a core EPS of $1.19 (including $0.05 benefit from the tax reform) against the expected $1.14. Net sales for the quarter were up by 3% against the year-ago figure while the gross margin slid by 60 basis points. The Republican tax reform brought in $135m in benefits costing a net charge of $628m. Cash flow from operating activities was $7.4bn.

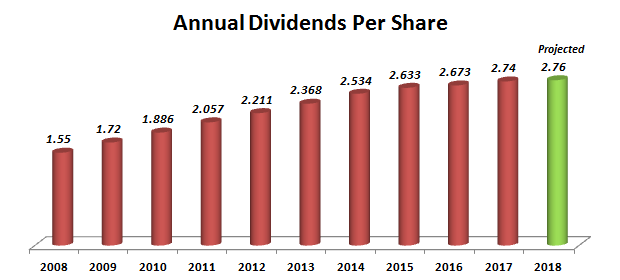

Across the Household & Personal Care sector, P&G has an attractive dividend yield of 3.44% and a 5-year growth rate of 4.77%. It has been paying a dividend for the past 127 years and has increased the dividend for 61 consecutive years. The current yield of P&G is higher than the average yield of the top 15 Personal products stocks which is at 1.93%. In Q2 2018, it repurchased $1.8bn shares and spent the same value in dividends, thus resulting in a total of $3.6bn returned to shareholders.

The dividend would increase in the coming years too as P&G has been adopting a robust cost-saving plan coupled with its re-focus on core brands post its brand divestitures since 2014 (the number of brands was reduced to 65 from 170). This uninterrupted distribution of dividend has partially offset the recent drop in the stock prices.

Why can investors be hopeful for P&G?

Prospective investors can be prudent to invest in P&G due to its core operating profit margin of 22%. Since the company has scaled down on its brands in the last five years, it has been able to focus on higher returns; and with competitive pricing, it has been able to improve its profit margin. Now, with the appointment of Nelson Peltz (effective March 1, 2018) to its Board of Directors after a long proxy fight, investors are hopeful for a greater impact.

Comparing it with its close competitor Unilever, P&G has a better Dividend yield and has a higher payout ratio. Unilever’s annualized dividend fell in 2015, while P&G has seen a sustained increase, thus making it a better stock in a prudent investor’s portfolio.

In order to fund its sales and continue its pace of growth, productivity improvements are essential. Its supply chain financing program has generated over $4bn in cash in the past four years. The management has saved $10bn in the past four years and has projected to save the same amount in the next four years- all in all- leading to sustained growth. The stock will see a sure turnaround if it continues this initiative.