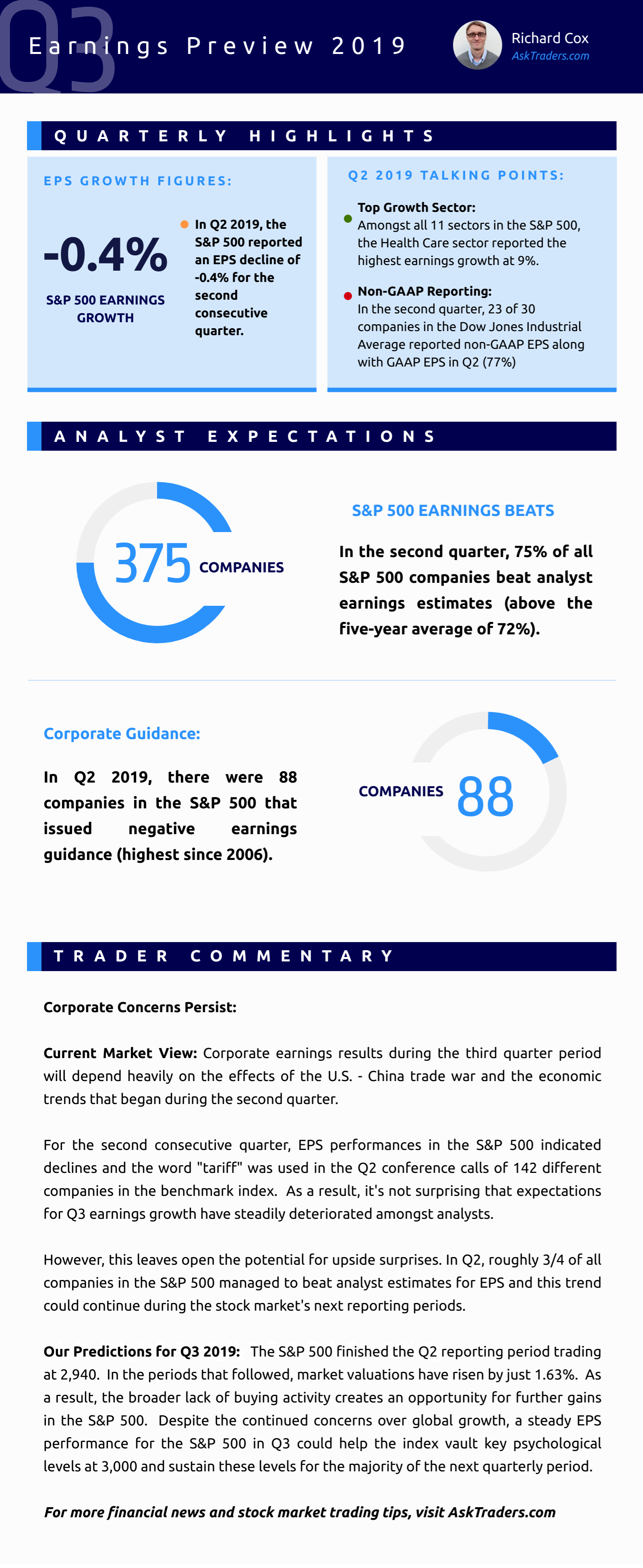

Current Market View: Corporate earnings performances during the third quarter period will depend heavily on trade war effects and the economic trends that began during the second quarter.

For the second consecutive quarter, EPS growth in the S&P 500 dropped and the word “tariff” was used in the Q2 conference calls of 142 different companies in the S&P 500. As a result, expectations for earnings growth have steadily deteriorated amongst analysts.

However, this leaves open the potential for upside surprises. In Q2, roughly 3/4 of all companies in the S&P 500, and this trend could continue during the next reporting periods.

Our Predictions for Q3 2019: The S&P 500 finished the Q2 reporting period trading at 2,940 and market valuations have since risen by just 1.63%. Despite the continued concerns over global growth, a steady EPS performance for the S&P 500 in Q3 should help the index vault key psychological levels at 3,000 for the majority of the coming quarterly period.

For more financial news and stock market trading tips, visit AskTraders.com

Citigroup: Stock Undeterred by a Hefty Tax Charge of $22 Billion

As a global banking leader for more than 20 years, Citigroup, Inc. (NYSE: C) posted a net income (on an operating basis) of $15.8bn in 2017 with an EPS of $1.28, 12% higher from 2016. This was the first time since the financial crisis of 2008 where earnings are more than their expectations.

The stock rallied to an all-time 10 year high of $80 on January 26, 2018. Total revenues in 2017 were up by 2%. Citi took a one time charge of $22bn (including $3bn in the repatriation of foreign funds) due to the Republican tax reform policy.

Citi stock is a favorite for shareholders and prospective investors as it has a steady EPS growth and is the cheapest of all banking stocks in the market. It is by far the largest of the top 10 banks in terms of EPS growth and P/E (according to Bloomberg Consensus). In terms of valuation, its stock is trading at a 22% discount and has a growing yield in its Corporate and Treasury bonds.

Source: Google Finance

With a good performance in 2017, it is now noticeable that Citi has come out the volatile period of revenue growth. Even after getting hit by a $22bn tax charge, Citigroup stock rose by 1%, as it delivered good performance excluding the charge. The new tax rate will give a boost to its profits.

Along with this, Citigroup CEO has reiterated on its promise of returning at least $60bn to investors in the next few years through buyback and dividends.

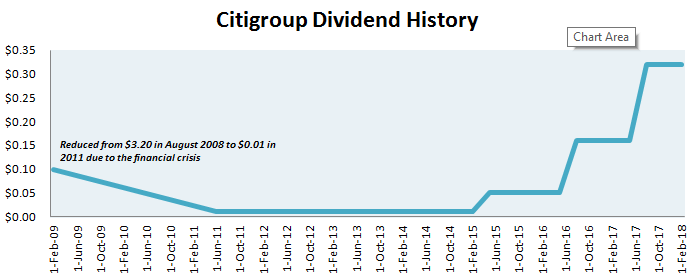

Citigroup Dividends: An Interesting Tale

Citigroup Dividend History

On January 18, 2018, Citigroup doubled its dividend of $0.16 to $0.32 after receiving Fed approval for its $15.6bn share buyback program. This is the largest ever share repurchase announced by Citi since its 2005 buyback of $15bn. In June 2016, Citigroup had boosted its dividends to $0.16 from $0.05 – a total three-fold rise.

Prior to the financial depression in 2008-09, Citigroup was known for paying high dividends to the tune of $5.4 per share. During the crisis, it slashed its dividend down to $0.1 in February 2009 and did not pay any till June 2011. Post this, it kept its payout at a minuscule $0.01 till 2015 when it finally raised it to $0.05. Its current dividend yield is 1.88% and shareholders can expect an upward momentum in his regard.

Where Does Citi Stand with other Top Banks?

Source: NASDAQ

Comparing Citigroup with Bank of America, both have performed well in terms of their stock rise in 2017. Citigroup has increased 15% while Bank of America has grown by 26%. Citi’s forward earnings multiple is less than 10 while BAC is at 11%. Both banks provide a decent dividend yield of more than 1.5%, with Citi’s slightly higher at 1.87%. This makes Citigroup a better buy.

The impending trade war due to Trump’s policy also had an impact on Citigroup shares due to its geographic exposures (it has banking licenses in more than 100 countries). Hence, its stock growth was down last year compared to JPMorgan Chase (NYSE: JPM) and Bank of America (NYSE: BAC).